Familial Identity Theft: When Your Child’s Thief Is Family (Part 1)

Kathryn Jones — Founder, The Identity Vault Kathryn built The Identity Vault to stop scams before they happen. Last Updated: April 2026 10 min read · Part 1 of 2 Part 1 of 2 When the Identity Thief Lives in Your House: A Parent’s Guide to Familial Identity Theft Key Takeaways 67% of child identity [...]

When the Identity Thief Lives in Your House: A Parent’s Guide to Familial Identity Theft

Key Takeaways

- 67% of child identity theft victims personally know their thief, according to Javelin Strategy & Research — and a parent or guardian is the single most common perpetrator.

- The motive is almost never malice. It’s usually a parent with damaged credit who tells themselves they’ll pay it back before the child needs it. They almost never do.

- Divorce and custody disputes dramatically raise the risk. An ex-spouse with access to your child’s Social Security number and a grievance is one of the most dangerous combinations in identity protection.

- The warning signs of familial identity theft look completely different from stranger theft — and most parents miss them because they’re watching for the wrong signals.

- If you recognize the pattern in your own family, do not confront anyone yet. Part 2 of this guide walks you through exactly what to do, in the right order, to protect your child without tipping off the thief.

In This Article

Familial identity theft happens more often than people realize. It happened to Axton Betz-Hamilton. Axton was 19 years old when she found out her credit score was 380. The clerk at the utility counter at the electric company asked for a $100 deposit to turn her college apartment lights on. She thought it was because she didn’t have any credit yet. Afterall she was just a college student with a couple of student loans and that was it. So when the credit report arrived in the mail a few weeks later in a thick envelope, ten pages single-spaced and full of credit cards and collection accounts she’d never heard of, her first thought was that there must be a lot of fine print.

There was just a lot of fraud. All of it had been opened in her name, starting when she was 11. It would take her another twenty years to find out who did it. What she discovered was the most common and least-discussed form of child identity theft in America. Familial identity theft was committed by someone inside her own home.

She would build an entire academic career studying child identity theft in the meantime — master’s degree, PhD, dissertation, a tenured faculty position. She became one of the country’s leading experts on the exact crime that had been committed against her, and she still didn’t know who had committed it. She suspected the same anonymous thief who had hit her parents in the 1990s. The family had moved. They’d gotten a P.O. box. The mail kept disappearing. Whoever it was had followed them. Familial identity theft had been the answer the whole time. They just didn’t know it yet.

In 2013, her mother died of cancer. A few weeks later, her father was going through her mother’s things in an outbuilding on the family farm and found a blue plastic file box. Inside it was a credit card statement in Axton’s name, opened in 1993, when she was 11. Her mother was the tax preparer and financial expert in the family. Axton’s pillar the one person she had called for help when her credit collapsed. Is the persond who had stolen her identity. Axton’s mother did not stop with Axton’s identity. She stole her husbands and and her father’s identities also. The person who had been sitting across from Axton at every Thanksgiving for nineteen years was the thief they’d spent two decades looking for.

This is the part of child identity theft almost nobody writes about honestly. The thief is usually somebody who lives in the house. If you’ve picked up on something in your own family that brought you to this article. It may be a feeling, a suspicion or a piece of mail you weren’t supposed to see. Your in the right place. What follows next is for you.

The Number Nobody Wants to Talk About

Most articles about child identity theft skip past the part where the thief is usually family. They mention it in a sentence and move on, because the rest of the article is easier to write if the villain is a faceless hacker. The number from Javelin Strategy & Research’s most recent child identity fraud study is hard to skip past once you’ve seen it: in 67% of households where a child has been a victim of identity fraud, the family personally knew the perpetrator. The single most common perpetrator is what researchers call a “parental figure” — a parent, step-parent, or a parent’s romantic partner. Other relatives and close family friends fill out the rest. For comparison, in adult identity theft cases, only about 7% of victims know who did it. Adults get hit by strangers. Children get hit by family.

This isn’t a statistical fluke. It’s the natural consequence of how children’s information moves through a household. A parent has the Social Security card, fills out the school forms, sets up the pediatric appointments, files the taxes. By the time a child is old enough to ask why someone is calling about a credit card in their name, that someone has had a decade of unsupervised access.

The structural problem has been documented for over a decade. The landmark Carnegie Mellon CyLab study of more than 40,000 American children found that more than 10% already had someone else using their Social Security number, making children roughly 51 times more likely to be identity theft victims than adults. The youngest case the researchers documented was a five-month-old. If you’ve ever wondered why the protection advice for child identity theft is so heavy on credit freezes and so light on “watch for suspicious strangers,” this is why. The threat isn’t a stranger. It’s almost always somebody who already has the keys.

Why Family Members Make the Best Identity Thieves

Picture a parent in serious financial trouble. A parent with maxed-out credit cards. Maybe they are behind on their mortgage payments. Parents who are suffering from an addiction or who have lost a job. Someone who has medical debt that has ballooned out of control. Their own credit is wrecked, so they can’t open a new card or even get the lights turned on. Then they remember that there’s a clean, unused Social Security number in the house, and it belongs to their seven-year-old.

What happens next is mechanically simple. The parent already has everything they need — a Social Security number they memorized when their child got their first passport, a birth certificate in a drawer, an address that’s also their address, the answers to every security question a lender has ever invented. From the lender’s perspective, the application is indistinguishable from a legitimate one, so it gets approved.

That’s the easy part. The hard part, if you’re the parent committing the fraud, is staying quiet. But staying quiet turns out to be easier than you’d think. The child isn’t watching their own credit. Why would they. They don’t have any reason to. If there is another parent in the picture there is no reason for them to check their childs credit. The statements arrive in a mailbox the parent controls. The minimum payment gets made just often enough to keep the account out of collections. The balance grows. Years go by. Nobody knows.

Most parents who do this aren’t thinking of themselves as criminals. They tell themselves the same story Linda Foley of ID Theft Info Source has heard at conferences for two decades: “I’ll pay all the bills, so by the time they turn 18, they’ll have great credit.” The intention may even be sincere in the moment. Unfortunatally the balance keeps growing. The minimum payments keep getting harder to make. Then before they know it one day the kid grows up.

It’s worth pausing here to draw a line that gets blurred constantly. Putting an asset into a child’s name as part of legitimate estate planning. Parents opening a 529 or setting up a UTMA account. Naming their children on a deed or gifting under the annual exclusion is normal financial parenting. None of that is identity theft. The line gets crossed when a parent uses a child’s Social Security number to take on debt the child becomes legally responsible for. Opening up any kind of liability in a childs identity such as a loan, credit card, car payment or a mortgage it familial identity theft. Gifting an asset gives the child something, while opening a credit account in their name gives them a liability.

Zach Friesen found out about that distinction the hard way. He was 17 and applying for his first student loan when the lender came back with a problem. There was already a $40,000 loan attached to his Social Security number. This loan had been taken out when Zach was 7,to finance a houseboat he had never seen. The loan had defaulted. The debt had been sitting on his credit report for a decade, growing in collections, while a parent told themselves they would handle it before he ever needed his credit. They unfortunately never did.

The Five Most Common Patterns

Familial identity theft tends to follow a small number of well-worn paths. If you recognize one of these in your own family, you don’t have to assume the worst. But you do have the responsibility to look.

The Bad-Credit Parent

The most common pattern by far. A parent has poor credit and uses the child’s SSN to open a credit card, finance a car, take out a loan, or set up utilities. Maryland’s Jimmy Louis Craighead is typical. Jimmy was convicted of using his three children’s identities ages 6, 4, and 2. Both Jimmy and his wife couldn’t qualify for credit on their own. He told the judge they needed it for food and fuel.

The Custody-Battle Ex

A divorcing or recently divorced parent uses the child’s identity as a weapon, a financial lifeline, or both. Family law attorneys see this constantly. One Virginia case documented by the Huffington Post involved a mother who used her daughter Diamond’s Social Security number to pass a credit check for an apartment. The father had to fight for years to clean it up, and the mother kept custody.

The Same-Name Parent

When a parent and child share a name (Junior/Senior, mother/daughter with the same first name), it becomes nearly impossible for credit bureaus to tell them apart. Ana Ramirez of Texas discovered her mother had used her SSN to take out a mortgage on a four-bedroom house when Ana was 10. They had the same first and last name, separated only by a different middle initial.

The Grandparent or Stepparent

The Javelin data is clear that biological parents aren’t the only perpetrators. Stepparents, the romantic partners of parents, and grandparents who have access to the child’s documents all show up in the cases. The bar is lower than people assume — anyone living in the household with the documents available can apply.

The “Helping Out” Relative

The mildest version, and often the hardest to confront of familial identity theft comes when an aunt, uncle, or grandparent uses the child’s identity. They tell themselves this is a short-term loan they’ll pay back, a car they need for work or a utility deposit. The damage is the same regardless of the intention.

Divorce, Custody, and the Risk Nobody Warns You About

If you’re in the middle of a divorce, or you’ve just finished one, this section is for you. A divorce creates the perfect conditions for familial identity theft. Two people who used to share everything — bank accounts, addresses, security questions, document access, the kids’ Social Security numbers — are now on opposite sides of a financial battle. Your ex knows your mother’s maiden name, the kids’ birthdays, where the Social Security cards are kept. And they may believe, fairly or not, that they have a moral right to whatever they can take.

This isn’t theoretical. Family law firms across the country treat post-divorce spousal identity theft as a routine concern, and when there are children involved, the children’s identities become a separate attack surface — one that’s even less monitored than the adult’s. A vindictive ex doesn’t have to use your credit. They can use your kid’s.

The legal system makes it harder, not easier. Police are notoriously reluctant to take a report when a parent uses their own child’s Social Security number. They view it as a domestic matter, a custody dispute, something for the family court to sort out. Many parents who’ve reported it to law enforcement have walked away with nothing. The HuffPost case of Diamond’s father describes exactly thisfr ustration documented fraud, a guilty plea, no jail time, no change in custody.

If you’re in a custody dispute and you suspect your co-parent has used your child’s identity, do not act on the suspicion alone. Part 2 of this guide walks through the specific order of operations — including when to talk to your family law attorney, how to document evidence without tipping off the other parent, and what to do when local police refuse to take the report.

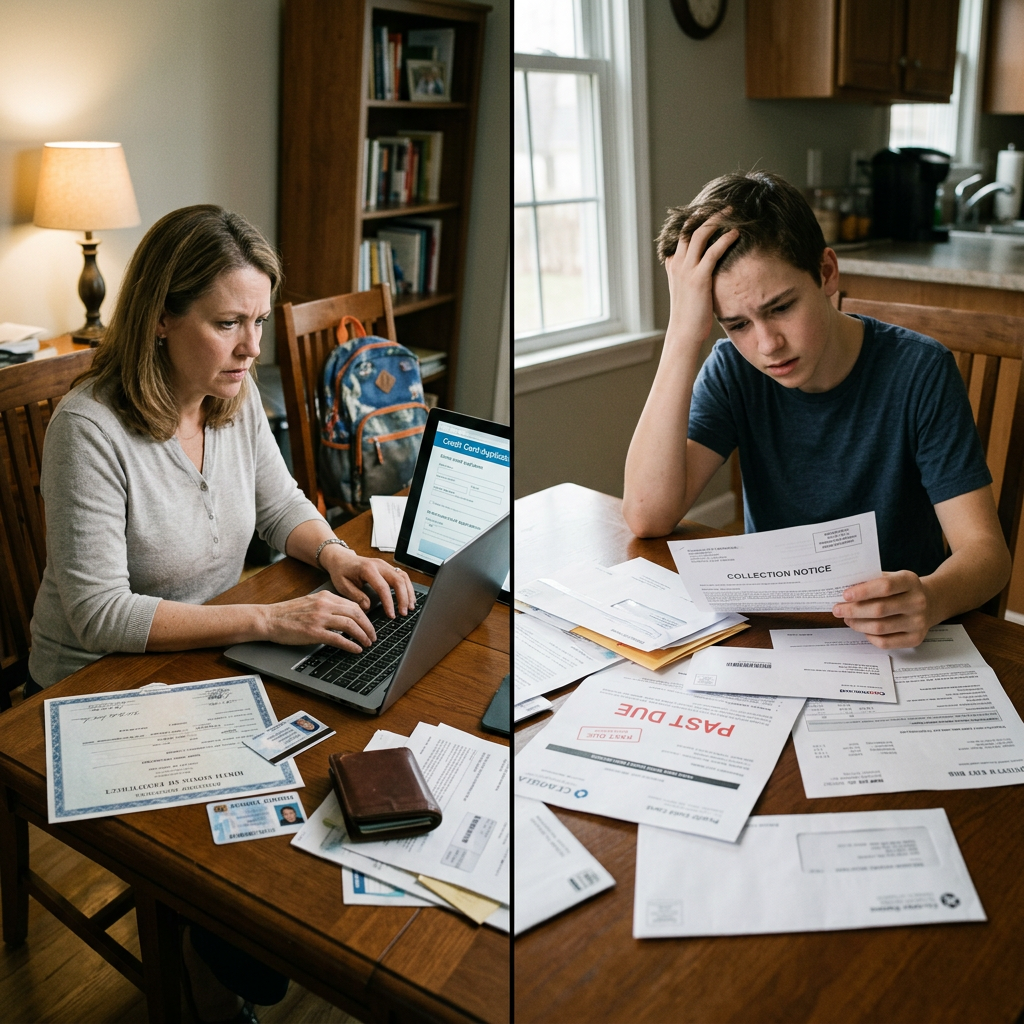

How to Tell If It’s Already Happening

The warning signs of familial identity theft look different from the signs of stranger theft. With strangers, the fraud usually shows up in places the family can see. Such as pre-approved credit card offers in the mail, collection calls, IRS notices. A family member who lives in the house can intercept all of those before you ever see them. Here’s what to actually watch for in the familial identity theft case.

Your child’s mail starts disappearing. This was the warning sign in the Betz-Hamilton case. Letters, magazines, even bills started vanishing from the mailbox before she was 11. The family got a P.O. box and the mail kept disappearing. The thief lived in the house.

Your child gets credit-related mail at a different address. A relative who’s used your child’s SSN to open accounts will often have the bills sent somewhere you can’t see. If you ever discover an old statement in a drawer that was sent to a different address — a relative’s house, a P.O. box you don’t recognize, a former family home — that is a serious signal.

A relative is unusually defensive about your child’s documents. If a parent, grandparent, or stepparent gets agitated when you mention freezing the child’s credit, requesting their credit report, or applying for an IRS Identity Protection PIN, ask why. The protective steps are free, easy, and have no downside. The only person who loses anything when a child’s credit is frozen is somebody who was planning to use it.

You discover credit accounts when trying to claim your child as a dependent. The IRS will reject a tax return that tries to claim a dependent whose SSN has already been used elsewhere. In custody situations, the most common explanation is that the other parent claimed the child first — but it can also be the trail of broader identity fraud.

A relative offers to “handle” anything involving your child’s SSN. Setting up bank accounts, opening 529 plans, signing them up for sports leagues, filing taxes. Most of the time this is just helpful behavior. Occasionally it’s the cover story for something else.

Your child’s school, doctor, or sports league reports a mismatch. When information doesn’t match what’s on file — a different address, a different birthdate, a name that’s slightly off — most parents assume clerical error. Sometimes it is. Sometimes it’s the trail of someone else using the same SSN under a different name.

If any of these signs are present in your family, the right next step isn’t to confront anyone. The right next step is to find out what’s actually on your child’s record.

Read That Carefully

If you suspect familial identity theft, do not confront the family member yet. The moment they know you’ve found out, they will start covering their tracks — closing accounts, shredding statements, intercepting mail. You need documentation first. Part 2 walks through exactly how to gather it without tipping off the thief.

What to Do Next

If you’ve read this far and recognized something in your own family. I want to say one thing directly you’re not crazy. The suspicion you’re sitting with is the most important signal you have. The reason this article exists is that almost nobody else is going to validate it for you. Family members will tell you you’re being paranoid. Police may tell you it’s a domestic matter. Friends won’t know what to say. The instinct to dismiss what you’re feeling is powerful. It’s the same instinct that lets familial identity theft go undetected for an average of seven years before anyone catches it. Trust the suspicion, then act on it carefully.

The protective steps work regardless of who the thief turns out to be. A credit freeze at all four bureaus stops a stranger or a parent equally. An IRS PIN blocks tax fraud whether the perpetrator is on the other side of the world or sitting at your kitchen table. The hard part of familial identity theft isn’t the protection itself. It’s knowing what to do first, what to do second, what to never do at all. Part 2 walks you through every step, in the right order, including the conversation waiting at the end of it.

Part 2 walks you through the recovery checklist, the legal mechanics, and the conversation nobody wants to have.

Read Part 2: What to Do When the Identity Thief Is Family →In the meantime, if you do nothing else this weekend, freeze your child’s credit at all four bureaus. It’s free, it takes about an hour, and it locks the door before anyone — family or stranger — can walk through it. Our free 30-step checklist helps you find the resources needed to secure yours or a loved ones identity.

Lock Down Your Family in One Weekend

A credit freeze at all four bureaus stops familial identity theft in its tracks — even when the thief lives in your house. Our free 30-step checklist walks you through freezing every bureau, securing your IRS account, and protecting your whole family in about an hour, completely free.